Chip shortage strengthening pricing policy of EU carmakers

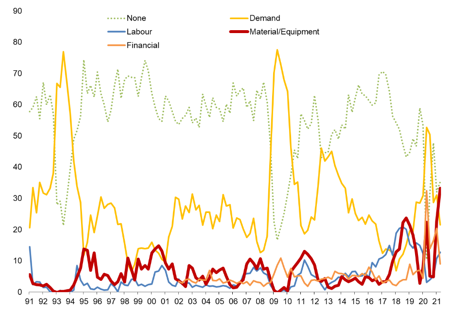

An unprecedented and worsening material shortage, especially in semiconductors, is creating a mismatch between supply and demand in the European automotive sector that could last until the first half of 2022. This gives automakers a unique opportunity to drop prices after nearly $ 20. increase of + 3-6% years of compulsions. In the first half of this year, the demand for new cars in Europe benefited from the grand reopening: new car registrations increased by + 25.2% compared to the first half of 2020 to reach just under 5.4 million of cars (+1.354 million units) (cf. 1) with clear double-digit growth in most countries, particularly in the top 4 markets (+ 14.9% in Germany, + 28.9% in France , + 51.4% in Italy and + 34.4% in Spain). This improvement is not yet sufficient to catch up with the pre-crisis volume, since 6.916 million cars (or +1.553 million units) were recorded in the first half of 2019. Nevertheless, it has already largely contributed to the improvement in the mood of companies in the sector, as shown by Eurostat business surveys on factors limiting production (see graph 2). Thus, the “demand” factor recorded a sharp drop in the 2nd quarter of 2021, going from the high levels of the 2nd and 3rd quarters of 2020 to the level of the 1st half of 2019, ie below the long-term average.

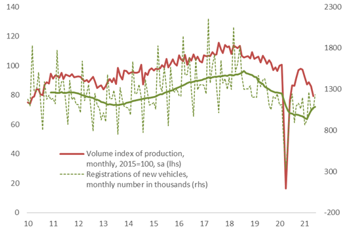

Figure 1 - Production and sales of new vehicles, EU-27

However, the same survey also points to a strong recovery of materials / equipment as a key factor in limiting production. The latter reached a record level in the second quarter, well above the previous records of 2018 and 2020, which was explained by regulatory developments in CO2 emissions and supply chain interruptions due to lockdowns. This historical scale of material / equipment shortages is closely linked to the Semiconductor shortage which has been exacerbated by the widespread adoption of just-in-time production processes among automakers aimed at minimizing the storage of all types of inputs. Also in the first half of the year, all car manufacturers stressed their obligation to optimize assembly lines, or even to reduce production.

In April as in May, the production volume index for the entire automotive sector at EU-27 level fell to its lowest monthly level since the early 2010s (see figure 1) - from -3.4% m / m and -7. 8% m / m - with most car manufacturing countries contributing to the decline, including the major ones. Against this background, the production level reached in May for the EU is still well below the pre-crisis level (-23% compared to the 2019 average), with established carmakers hit the hardest (- 33% for France, - 30% for Germany, - 25% for Spain and -10% for Italy) than for other manufacturer countries such as the Czech Republic (-6%), Sweden (- 6%) and Hungary (-5%).

Figure 2 - Factors limiting production in the automotive sector, EU-27 level, quarterly survey

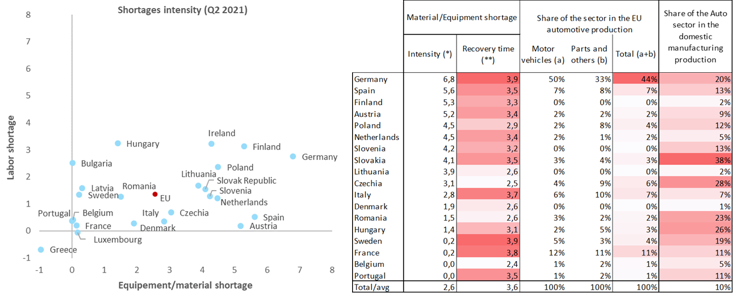

Looking at past episodes of material / equipment shortage, the intensity of the restriction reached in the second quarter of 2021 appears to be 2.5 times the standard deviation observed in Europe in the past. This intensity of scarcity is particularly pronounced for Germany and Spain (i.e. 51% of EU production) and, to a lesser extent, in small car-producing countries such as Finland, the Netherlands and Slovakia (see figure 3). The differences in scarcity intensity reflect different demand expectations (which led to different order reductions), unequal supplier relationships (short term vs. chips (chip shortages are more important to managing the supply chain). power supply and microcontrollers only for Advanced Driver-Assistance Systems products).

We calculate that it could take an average of 3.5 quarters for the current bottlenecks to normalize, with Germany and Sweden having to wait longer (3.9 quarters each, see Figure 3). In the best-case scenario of a recovery that begins as early as Q3 2021 - this is the time most cited by automakers today - we estimate that the recovery process will be completed in Q2 2022.

Interestingly, the recovery time is longer in Western Europe: Germany, Sweden, Spain and Italy, which together account for 72% of EU production, will take more than 3.5 quarters to recover, while Hungary nearly three quarters and the Czech Republic, Poland, Romania will need it and Lithuania less than three quarters.

Figures 3a & 3b - Bottlenecks by country, EU-27 countries, 2nd quarter 2021

(*) in number of standard deviations observed over the last twenty years

(**) in number of quarters

Sources: Eurostat, Euler Hermes, Allianz Research

The prolonged scarcity will maintain a mismatch between supply and demand in Europe until the first half of 2022, as domestic demand fundamentals remain better aligned in the short to medium term. There are several reasons for this: some are directly related to the grand reopening, such as building consumer confidence and releasing significant amounts of it (partially).

Household savings

. Others are specific factors influencing the purchase of cars with international internal combustion engines and, from 2022, the need for car rental companies to modernize their fleets.

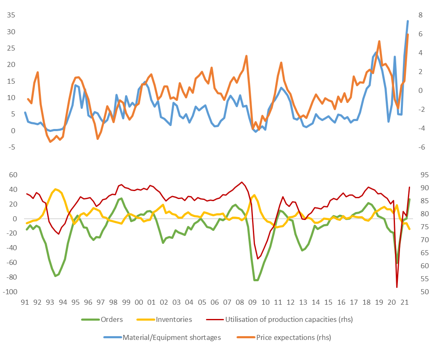

At the same time, we don't expect exports to ease the mismatch between supply and demand, as the US market is experiencing stronger momentum (with vehicle sales already close to H1 2019 levels. (8.5 million units), which is expected to affect the automakers that export the most to the American brands, especially German. According to business surveys, domestic and export orders have already reached levels record in June, which bodes well for demand prospects for the coming months (see Figure 4) - provided the health situation remains under control.

Figure 4 - Company sentiment on bottlenecks (materials / equipment), price expectations, orders, stocks and production capacity utilization, EU-27

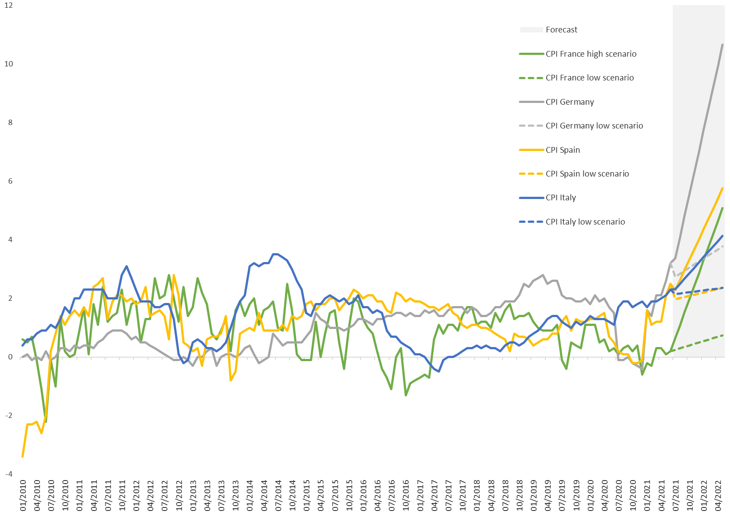

In this context, we expect car prices in Germany to increase by at least + 4% with a potential of over + 10%. Spain and Italy could see an increase between + 2.4% and + 5.8%, while France could see an increase between + 0.8% and + 5.0%. Unlike in the past, the automotive industry today is faced with a unique supply situation in which all the stars are aligned: a very large order book, a very high utilization of production capacities, which reflect the strong adjustments of industry due to the pandemic, and very low inventories at a time when companies are faced with rising prices for raw materials (rubber, copper, steel) and higher freight rates.

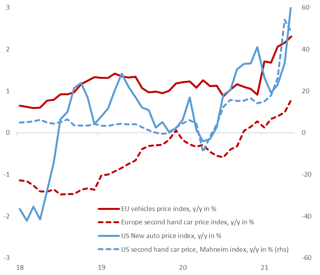

This unique context promotes a higher level of transmission to the consumer, also because it "helps" automakers to repeatedly align their product line in favor of the most profitable cars in favor of the premium segment - and therefore German brands. The financial reports available for Q1 and Q2 2021 confirm good, if not strong margins in most cases, despite lower volumes. This context also implies an upward trend in used car prices in Europe, but not of the order of magnitude in the United States, the American market having proved to be much more massively constrained by supply (lower record as of May 2021).

Figure 5 - Price development of new and used cars, EU-27 and US

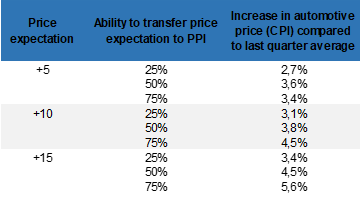

To get the estimated price increase, we calculate the elasticity of the car CPI relative to the car PPI during periods of recovery to capture the historical pace of the recovery. Next, we describe a set of scenarios (see Figure 6) based on (i) three levels of price anticipations and (ii) three levels of transmission capacity to have a number of potential price increases with both cases extremes:

A “low” scenario in which car manufacturers' price expectations are lower (+5 basis points) and their pricing power is low (25%).

The “high” scenario in which car manufacturers' price expectations are still high (+15 bps) and their pricing power is high (75%).

Next, we simulate the effects of the expected price shock by adding it to the average of the last three months. Finally, we distribute the simulated shock on the CPI over the recovery time.

Figure 6 - Potential increases in car prices, EU-27 level

The potential increase in vehicle prices may differ slightly from country to country (see Figure 7). In Germany, which represents almost half of the automotive sector (44% of production and 38% of registrations), we expect car prices to increase by at least + 4%, but with a potential of more than + 10 % already in the year Started to increase in 2021 (+ 2.6% y / y in May and + 3.2% y / y from June). Spain and Italy, which both account for 7% of the production of the automotive sector, are expected to increase the price of their cars between + 2.4% and + 5.8%. In France, whose prices have been more stable in the past, the prices of its cars should increase between + 0.8% and + 5.0%.

These figures should be put into perspective with the maximum automotive CPI observed in the past: + 2.8% for Spain, + 2.9% for France, + 3.3% for Germany and + 3.5% for Italy. In our “low” scenario, we assume that only the CPI for German passenger cars would be above its historic level. In our “high” scenario, we estimate that the four countries - accounting for 2/3 of EU car production - would have a historic pace in terms of passenger car CPI.

Figure 7 - Potential increases in car prices, selected countries

Edited (c)

Source: ACEA, Eurostat, Euler Hermes, Allianz Research